Sponsored Content

In the second part of his series, Tim Townsend, head of wealth management and corporate consulting at Alexforbes Offshore, outlines the third and fourth steps in the journey to financial wellbeing

LAST month I wrote about the concept of financial wellbeing and how we can all relate to this as we forge our way through life, often focused on our current self.

Feeling better about money and being resilient, confident, empowered and in control is the end goal. It’s fair to say that all the aforementioned would impact our overall wellbeing and happiness, which is why this is a topic so close to my heart.

As we each learn how to better understand our relationship with money and define what it is we want out of life (and what that will cost us, ie. our lifestyle) we can start to shift our focus from living for today to keeping an eye on the future. Sometimes that means looking out decades into the future and the dreaded R word creeps up… yes, I am not going to say it as I know you won’t read on past this paragraph, so we will save that for next month.

Typically, this is the precise mindset which so many follow when it comes to planning for the future, so let me take things one step at a time.

Once we are on top of the day-to-day (and we all face the challenges of the consumer-driven society we live in today), we can start to think about tomorrow, then next month and, dare I say it, next year. Therefore, let us take this one step at a time.

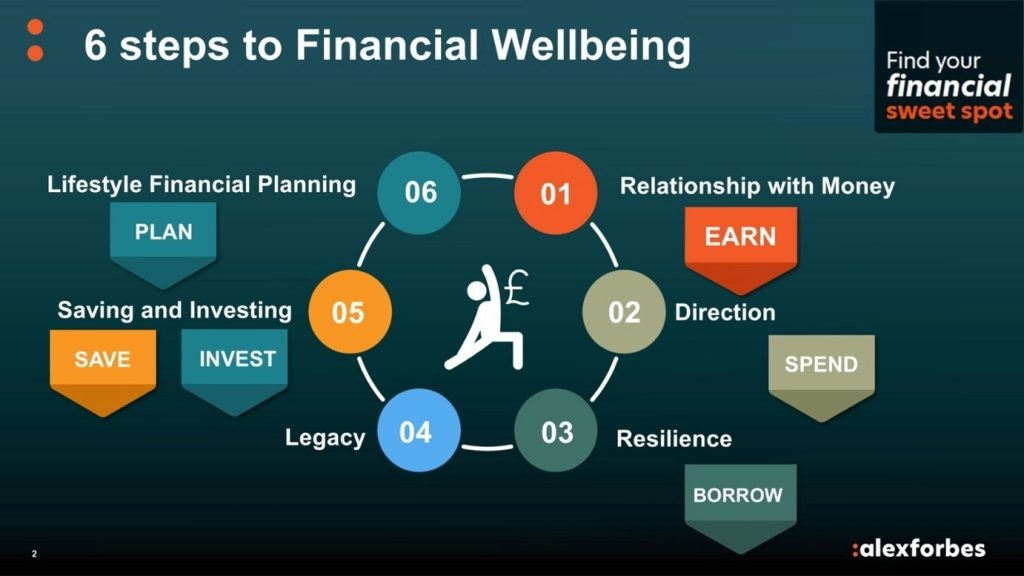

Over time, we develop these day-to-day money behaviours and understanding about how to make better decisions around the way we earn, spend, borrow, save and invest. These are all behaviours we must work on improving before we can start making progress on a longer-term financial plan.

This is not easy and many of us can get stuck in the now. This often leads to a key middle step being missed. What I am referring to is developing the next step.

Step 3: Resilience

What we mean by this is “what would happen if the curve balls in life come flying in”?” What happens if your washing machine gives up the ghost? (No reference to Halloween here, folks, but this is scary stuff we are talking about.).

Emergency Fund: What happens if the Grim Reaper rudely pays you a visit before the mortgage is boxed off? This is a bigger conversation, as there may be wider protection needs to consider as, if you can’t work (yes, that first behaviour = earn) for an extended period of time, then who will pay the mortgage?

This leads us to income protection. Unsurprisingly, this concept of protecting ourselves against a future uncertainty or accident is not all that foreign to us. What happens if we drive into someone on the way into work?

Life Insurance. This is why I walk into work, possibly one of my favourite parts of living in Jersey. While we all have car insurance, start thinking about potential risks beyond today and that’s where we see a gap emerging. What if we get really sick? Yes, the C word springs to mind. This is a life-altering event. We, and those around us, change during and after our battles to return to health, leading us to the topic of critical illness cover.

There are multiple pieces to the overall resilience puzzle, but it does mean thinking beyond today. If you don’t, your plan could be derailed or you could find yourself leaning on a credit card or personal loan to get you through the tricky time or curve ball and, frankly, those credit cards are like quicksand… you get stuck or trapped and can’t move forward onto steps four, five and six of your journey to better financial wellbeing.

UK statistics show that only half of us view life insurance, income protection and critical illness as important. The reality is that over a quarter of those who had no protection conversation when taking a mortgage said they would have been interested.

In the UK, 57% of consumers surveyed by the Association of Mortgage Intermediaries did not own any protection policy. This is not a one-off. Just as we review our car insurance annually, we should regularly review our protection needs as life changes, our circumstances change and so do our risks. It is a fundamental conversation to have with your financial planner.

Step 4: Legacy

Now, the Grim Reaper has already made an appearance in our Halloween edition of the six steps financial wellbeing series. I’m not trying to spook you here or scare the life out of you, but we owe it to our families to put a plan in place should we make an early exit. It comes earlier for some than for others, and this is another tricky part of life.

Ensuring you have clarity on what happens to the loved ones and assets you leave behind is key. Whether it is that pension pot you have as part of your work benefits that needs to be earmarked for a spouse or partner, cash savings or investments or your home, you need a will to cover everything you accumulate here in Jersey.

And this is twice as important in Jersey as it is anywhere else because you need two wills, one for the stuff that you can pick up and move around (movable assets), and another for those that are not going anywhere (immovable assets such as property).

But the planning doesn’t stop here. In this increasingly digital age, we need to manage the footprint we leave online. This relates to our digital assets, which include our memories and life catalogue on social media. We all tend to live up in the cloud before we eventually move up into the clouds for good.

All of this requires thought and planning and a regular check-in as things change.

Now, as we get older, we may be fortunate enough to have accumulated a few of these movable and immovable assets, so we can plan what we pass down to family and what goes to charity. As time marches on and we get closer to meeting Grim, we tend to think more about the legacy we leave behind.

The recent passing of Simon Boas and the legacy he has left behind in his book “A beginner’s Guide to Dying” offers a new perspective on the inevitable event that faces us all. It also offers some perspective on living a life full of joy.

I think we can all relate to that and, if chipping away at the six steps to our financial wellbeing helps to enable this end goal, then it is all worth it in the end. If the “why” behind managing our money was to enable more moments of joy and happiness, then our mindset would change around the topic of our personal finances.

Simply put, we are trying to fund our own version of happiness, for today and tomorrow. If that is something you need a bit of help with, click here to take our Money Storytypes quiz to get your started on your journey and please do not hesitate to reach out to us at advice@alexforbes.je.