Sponsored Content

Harry Brassington, of Team Asset Management, offers this week’s market review

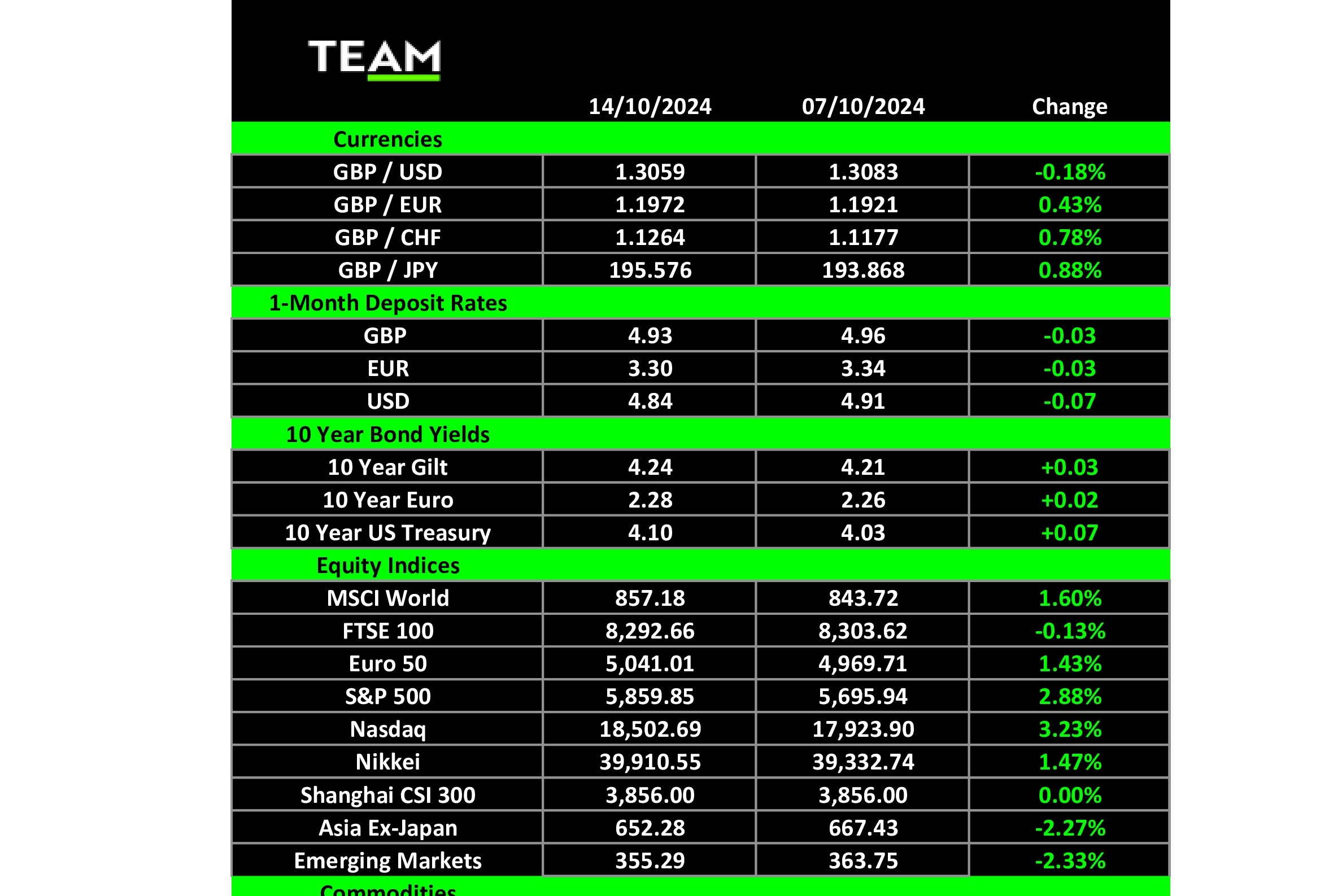

The 2024 bull stampede continued in earnest this week, with all major US indices, the Dow Jones Industrial index, the S&P 500 index, and the technology-laden Nasdaq index, producing gains of over 1%. At the time of writing, the bellwether S&P 500 index is enjoying its best start to a year this century.

Hallmarks of an impressive bull market include its ability to climb the proverbial “wall of worry”. As we head towards the final straight this year, US employment data, the US election, and the next Federal Reserve Committee meeting all zoom into view.

This may underpin the steady rise in the VIX index lately. The VIX level, also known as Wall Street’s “fear gauge”, as it measures the appetite of investors to buy near-term portfolio insurance, has been above 20 most of the week. This is a level that ordinarily points to more jittery markets, but the US has powered on, ostensibly on good third-quarter earnings results from financial titans JP Morgan and Wells Fargo.

Recessionary fears remain very real in the Eurozone, with France and Germany reporting rather lacklustre economic figures. LVMH was in the headlines last week following their merger activities; however, low demand from their biggest customer, China, could be a drag. News like this ups the ante for an ECB rate cut that was until now not on the horizon a month ago – but life comes at you fast!

Against a backdrop of major financial stimulus announced by the Chinese government, Chinese stocks staged a rebound that saw them end the week higher. Volatility is certainly the flavour of the market as the market swung between gains and losses. This is nothing new as we have seen in the space of a fortnight a 52-week high, and a 52-week low posted. These price moves all underscore the cautious optimism surrounding the market while details of the economy-boosting measure are revealed.

Closer to home, the UK is hosting a major investment summit in London in the hopes it can attract big sums of investment.

True to form in these early days of Labour government rule, plans rarely go without a side story. The latest was a spat with the owner of P&O ferries who were branded a “rogue operator” by Transport Secretary Louise Haigh, who requires a cool £1bn to develop the London Gateway. However, after a public dressing down and much schmoozing, they are back at the table and a promise of creating more than 400 domestic jobs.

The UK desperately needs to balance its budget plans with its investment plans. The tax policies needed to balance the books are the very thing making the UK look like an unattractive place to do business. The PM and Rachel Reeves have already warned that the budget will be painful and dreaded tax rises may be unavoidable. The big day is Wednesday 30 October, when we will get our first glimpse of just how balanced the UK will be.

In the US, earnings season was kicked off by the big banks. Earnings season is closely watched not just because of the share price, but it’s also a great litmus test for the wider economy. Good earning equals a good economy.

Bank of America shrugged off news that Warren Buffet’s Berkshire Hathaway has trimmed its shares in the company. Under listing rules, if you own more than 10% of a listed stock you are required to make regulatory disclosures. Berkshire is now below this limit, and the Sage of Omaha no longer needs to tell the market what he’s doing with this stock.

Boeing continues to struggle with its PR, with workers striking over their latest pay deal. The firm has tabled a 30% increase, but the workers are holding fast for a 40% increase. Meanwhile, they have had a dressing down from the largest international airline, Emirates. Further delays to new models have warranted a “serious conversation”.

The outcome of the US election is anyone’s guess at this stage. The polls this week have seen a meaningful swing in favour of Donald Trump. Ultimately, the margin of error suggests a narrow victory for either candidate. But the polls only show the popularity of a candidate, what counts is the Electoral College, where the weight of “swing” states counts more than popularity.

A Trump White House is usually good for markets, as he spends in areas that the markets like but drives up debt. A Harris White House would spend money on social policies. Regardless, the seemingly growing and unchecked, mountain of US debt will need to be addressed at some point in the next campaign.

Looking to the week ahead, US corporate earnings season will take centre stage. Estimates have been revised downwards, or managed if you are more sceptical, to levels that should facilitate positive surprises. Goldman Sachs, Johnson & Johnson and Bank of America are likely to set the tone.